How Austin's Expanding Flood Zones Are Hitting Homeowners' Insurance and Mortgages

A neighborhood-by-neighborhood guide to where the lines are moving, what it costs, and what you can do about it

How Austin’s Expanding Flood Zones Are Hitting Homeowners’ Insurance and Mortgages

A neighborhood-by-neighborhood guide to where the lines are moving, what it costs, and what you can do about it

If you bought a home in South or Northeast Austin in the last five years, there’s a real chance the map your lender used at closing no longer matches the map your insurance company is looking at. Add the city’s separate map to the mix and things get complicated fast. Austin sits inside one of the most tangled flood mapping jurisdictions in Texas. A federal map and a local map coexist, sometimes disagree, and each can trigger separate, expensive obligations.

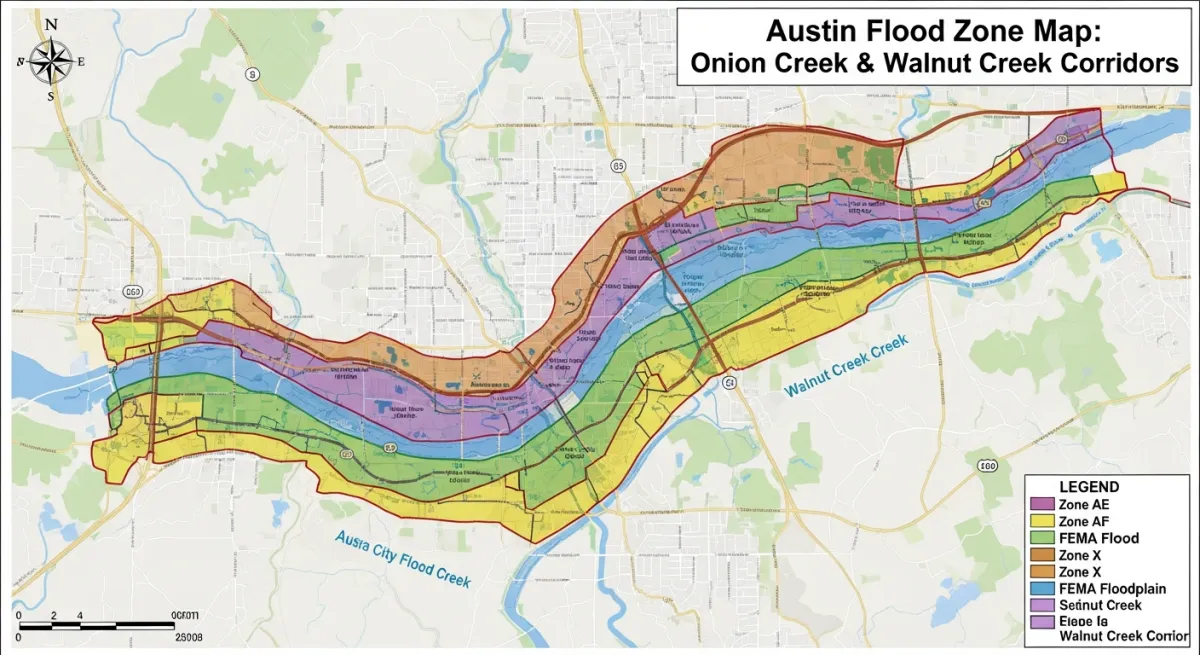

FEMA keeps updating its Flood Insurance Rate Maps. Austin’s Watershed Protection Department maintains an entirely separate set of more restrictive floodplain boundaries. Homeowners and buyers in corridors from Onion Creek in the south to Walnut Creek in the northeast are learning about both systems the hard way—usually at the closing table or on a renewal notice, when there’s the least time to do anything about it.

Here’s everything you need to know before that happens to you.

The Map Your Lender Is Looking At, and Why Austin Has Two of Them

Most homeowners have heard of a FEMA flood map. Fewer know the City of Austin maintains its own Fully Developed Floodplain maps, which are more conservative than FEMA’s Flood Insurance Rate Maps. The city calls them FIRMs. It uses them to govern local permitting decisions. The two systems serve different masters and often return different answers for the same address on the same day.

FEMA’s FIRMs are what your lender and your federal flood insurer look at. They define Special Flood Hazard Areas—SFHAs—which are zones with a 1-percent or greater annual chance of flooding. People commonly call this the “100-year floodplain,” which has always been a slightly misleading label, but that’s a separate argument.

Zone designations on a FIRM break down like this:

Zone AE is the standard high-risk designation. FEMA has calculated a Base Flood Elevation—the BFE—for these areas. That’s the elevation floodwaters are expected to reach in a 1-percent annual chance flood. This is where mandatory purchase requirements kick in, where insurance costs the most, and where lenders scrutinize closing files most carefully.

Zone A also counts as an SFHA subject to mandatory purchase requirements, but without a calculated BFE. It’s an older or less-studied designation, more common in areas FEMA hasn’t yet fully modeled.

Zone X sits outside the 500-year floodplain, or between the 100- and 500-year boundaries in the shaded variant. No mandatory insurance purchase requirement here, and preferred-risk rates apply if you want voluntary coverage.

The City of Austin’s Fully Developed Floodplain maps model what the floodplain would look like if every undeveloped acre in a watershed were fully built out with impervious cover. You can access them through the FloodPro GIS viewer at austintexas.gov/floodpro. The city uses this more conservative calculation for permitting and land-use decisions. A parcel can sit in the city’s floodplain—facing real restrictions on what you can build or remodel—even if FEMA has it in Zone X. Your lender doesn’t use FloodPro. The city’s planning department does, and you should too before you start drawing up plans for a bathroom addition or a detached garage. As we cover in our home & property coverage, decisions like these have lasting effects on what your home can do for you financially.

The FEMA Flood Map Service Center is at msc.fema.gov. Both tools are free and publicly accessible. The differences between what they show for any given parcel can be significant enough to affect what you can legally do with your property. Pull both before making an offer on anything near a creek corridor.

Where the Lines Are Moving Right Now

Onion Creek (78748, 78744, 78747)

Onion Creek is ground zero for Austin’s flood zone reckoning. The corridor stretching through South Austin flooded repeatedly before October 31, 2013. A Halloween night storm sent water into hundreds of homes. That event, combined with the Memorial Day 2015 floods that hit central Texas watersheds, led to one of the largest city-funded voluntary buyout programs in Austin history.

The City of Austin’s Onion Creek buyout program acquired somewhere around 800 to 900 parcels in the most dangerous portions of the floodway and floodplain. The homes are gone—now parkland or open space. But the flooding risk that generated those buyouts also drove successive FIRM panel revisions that pulled neighboring properties into Zone AE. Some owners who thought they were fine suddenly weren’t. Austin’s Watershed Protection Department processed multiple Letter of Map Revision filings in the Onion Creek corridor over the past decade.

If you purchased in these ZIP codes before a panel revision and your title work shows Zone X, pull your current FIRM panel number at msc.fema.gov and confirm that designation is still current. Panel effective dates matter: a map letter dated before FEMA’s most recent revision isn’t a reliable indicator of where you stand today.

Walnut Creek (78753, 78754, 78727)

Northeast Austin’s Walnut Creek corridor presents a different problem. Onion Creek’s risk comes from the Edwards Plateau’s ability to deliver catastrophic runoff from short, intense storms. Walnut Creek’s expanding floodplain is driven by development—the steady accumulation of impervious cover from rooftops, parking lots, and roadways. Over the past fifteen years, the watershed has absorbed enormous growth. The land simply doesn’t absorb water the way it used to.

As impervious cover increases, the same rainfall event produces more runoff, faster, with less infiltration. Hydrological models underlying FIRM panels account for existing impervious cover, but in a rapidly developing watershed, modeled conditions can lag actual conditions by years. Austin’s Watershed Protection Department flagged Walnut Creek as a corridor where development-driven runoff increases are pressuring map revisions. Properties in the 78753 and 78754 ZIP codes saw expanded Zone AE delineations in recent revisions, including Rundberg-adjacent neighborhoods and portions of the North Lamar corridor.

Buyers shopping in these areas should verify a flood determination letter against the most current FIRM panel at the Map Service Center. Don’t rely solely on the determination company’s internal database, which can lag revisions by months. Development activity is ongoing, which means older determination letters may not reflect the most recent panel changes.

Shoal Creek, Boggy Creek, and the Colorado

Shoal Creek through Central Austin and Boggy Creek through East Austin have been under ongoing city and FEMA modeling work. This includes the 78702 and 78722 ZIP codes—some of the most sought-after real estate in the city right now, which makes the flood exposure easy to underestimate.

Shoal Creek runs through Hyde Park, Brentwood, and the North Loop area before emptying into the Colorado. The 1981 Halloween flood and the 1988 Mother’s Day flood both caused serious damage to properties in these corridors. Those aren’t historical curiosities—they’re documentation of what the creek does when conditions line up. Properties along the Colorado below Longhorn Dam carry Zone AE designations that were updated in the early 2020s.

The Watershed Protection Department at 512-974-2550 is your most reliable local contact for current panel status, pending preliminary revisions, and what’s in the pipeline for any of these three systems. FEMA typically issues preliminary maps before they take effect, which gives property owners a window to comment, appeal, or pursue LOMAs before new designations lock in. Missing that window is expensive.

How to Look Up Your Address Before Your Lender Does

Start at msc.fema.gov. Enter your property address. The tool returns your current FIRM panel number—a nine-character code identifying the specific map tile—and your flood zone designation. Write down the panel number and the effective date. Those two pieces of information tell you whether you’re looking at a recently revised map or a stale one.

Next, look for the “Pending Changes” indicator. FEMA’s MSC will flag if a panel has a preliminary revision in progress. The current designation may be about to change, in either direction. If a LOMA has been issued for your specific parcel, the MSC should reflect it.

Then open austintexas.gov/floodpro and search the same address. Note where the city’s Fully Developed Floodplain boundary falls relative to your structure. If it places any part of your lot in the floodplain—even if FEMA does not—you’ll face local permitting restrictions on improvements. This is not a federal lending issue. It’s a real constraint on what you can do with the property.

The two tools disagree sometimes. Remember which one controls what: FEMA’s FIRM controls federal lending and NFIP insurance eligibility. The city’s FloodPro controls local permits and development standards. You can be in the clear for a mortgage and simultaneously restricted by the city from adding a room. I’ve talked to homeowners who were blindsided by exactly this—they had no lender requirement and assumed that meant no flood-related constraints at all. It doesn’t.

What Flood Insurance Actually Costs Here

FEMA’s Risk Rating 2.0 took effect for new policies in October 2021 and for renewals in April 2022. It changed how the National Flood Insurance Program prices risk. The old system tied premiums almost entirely to your FIRM zone designation. The new system incorporates your property’s specific risk factors: distance to water, type of flooding, first-floor elevation relative to BFE, and the cost to rebuild. Two houses on the same block in Zone AE can now pay very different premiums. That’s a more rational system—but it also means you can’t ask your neighbor what they pay and assume it applies to you.

For Austin-area properties, local independent agents who write NFIP policies in the Onion Creek corridor report annual premiums for Zone AE properties running from roughly $2,000 on the low end to $5,000 and above, depending primarily on how the first-floor elevation relates to Base Flood Elevation. A home elevated two feet above BFE pays dramatically less than one sitting at or below it. That differential—documented on an Elevation Certificate—is the single most important variable in your premium. Zone X properties with preferred-risk policies have historically paid well under $1,000 annually, often in the $400–$700 range, though Risk Rating 2.0 has introduced more variation even at the lower end.

Here’s what catches people: the NFIP caps residential building coverage at $250,000. In a city where median home values in many neighborhoods have crossed $500,000, that cap creates a serious problem. A Zone AE homeowner can be fully compliant with their lender’s requirements and still dramatically underinsured for a catastrophic loss. The NFIP’s contents coverage cap adds another $100,000 for residential properties. Do the math on your own home and sit with that gap for a minute.

The private market exists to fill it. Carriers writing flood policies in Austin include Neptune, Wright Flood, and Selective. Private policies can offer higher coverage limits, shorter waiting periods (the NFIP imposes a standard 30-day wait, which is its own problem if you’re buying in a hurry), and sometimes lower premiums for moderate-risk properties. But local agents report that private carrier appetite has narrowed in the highest-risk Austin ZIP codes—particularly the Onion Creek corridor—following the 2013 and 2015 loss events. In a high-risk corridor, the NFIP may be your only real option, which makes the $250,000 cap considerably more serious than it would be somewhere you have alternatives.

The Mortgage Problem

Federal law requires flood insurance on any structure in a Special Flood Hazard Area that carries a loan backed by a federally regulated lender. This captures nearly all conventional mortgages sold to Fannie Mae or Freddie Mac, as well as FHA, VA, and USDA loans. If your property is in Zone AE or Zone A at closing, you will be required to show flood insurance as a condition of closing. Not discretionary.

The Biggert-Waters Flood Insurance Reform Act gives lenders 45 days to notify a borrower after a map revision places their property in an SFHA. If you don’t obtain a voluntary policy within that window, the lender can force-place coverage on your behalf and charge you for it. Force-placed flood insurance protects the lender’s interest, not yours. Rates typically run two to five times what you’d pay for a comparable voluntary NFIP policy. Coverage is structured around the lender’s collateral, not your equity. You have limited control over terms. Maintaining a current voluntary policy is one of the most straightforward financial protections available to owners in affected zones—and one of the most commonly ignored.

For jumbo loans—increasingly common at Austin’s price levels—lender requirements vary by institution. Jumbo products aren’t sold to Fannie or Freddie, so they’re not technically subject to the federal mandatory purchase requirement in the same way. Most jumbo lenders impose their own flood insurance requirements for SFHA properties anyway; they’re carrying the whole-loan risk themselves. Austin mortgage brokers reported deals stalling when Risk Rating 2.0 premium quotes came back significantly higher than buyers expected, particularly on higher-value properties in Onion Creek where the gap between the NFIP’s $250,000 building cap and the home’s actual value forced supplemental private coverage the buyer hadn’t budgeted for.

One scenario that catches buyers off guard: properties that were Zone X when the seller bought them but have since been remapped to Zone AE. The seller has no flood insurance. No policy history to transfer. The buyer’s lender pulls a flood determination, identifies the new zone, requires insurance, and the premium quote lands somewhere in the $3,500–$5,000 range—a full Risk Rating 2.0 rate with no grandfathering. The buyer assumed the property had no flood exposure. That’s a material change in carrying cost that should affect purchase price negotiations. On deals with tight debt-to-income ratios, it can kill the purchase entirely. Local agents say it’s happening more than buyers realize.

If the Map Just Changed on You

If your property was remapped into Zone AE and you believe the designation is wrong, you have administrative remedies. Maybe your land is actually higher than FEMA’s model reflects. Maybe fill was placed on the property after the original mapping. It’s worth checking before you accept the new designation and start writing checks.

A Letter of Map Amendment (LOMA) removes a specific property or structure from the SFHA based on natural ground elevations. If your lowest adjacent grade—the ground immediately next to your foundation—is at or above BFE, you may qualify. A licensed surveyor provides the elevation data; you submit the application to FEMA. If approved, the LOMA officially removes your property from the zone, which eliminates the mandatory purchase requirement for federally backed loans. You can typically drop the NFIP policy if you choose, though that’s a separate risk decision worth thinking through.

A Letter of Map Revision Based on Fill (LOMR-F) addresses a different situation. If fill was placed on your property after the original FIRM panel was published, a LOMA may not apply—FEMA’s mapping may already reflect the natural grade. The LOMR-F process covers this specifically. It’s more involved than a LOMA and may require documentation of when the fill was placed and by whom.

Before pursuing either—and before accepting your first NFIP premium quote as final—get an Elevation Certificate. A licensed surveyor in Austin typically charges $500 to $1,000. The EC documents your first-floor elevation relative to BFE. If your first floor is above BFE, even slightly, your NFIP premium should reflect it under Risk Rating 2.0. If it’s significantly above BFE and your lowest adjacent grade is also above BFE, the EC is the foundational document for a LOMA application. That surveyor fee can pay for itself many times over in reduced annual premiums. It’s one of the better investments a Zone AE homeowner can make. If you’re weighing it against other property upgrades, our coverage of home improvements that add resale value in Central Texas puts that cost in useful context.

Grandfathering rules also matter if you already have an NFIP policy. When your zone changes, federal rules protect you from an immediate rate reset—FEMA has held annual increases to 18 percent for primary residences in most circumstances rather than allowing an immediate jump to full Risk Rating 2.0 rates. A continuous NFIP policy has real financial value even when you’d rather not be paying for one. When a property sells, the new buyer does not inherit grandfathered status. They pay Risk Rating 2.0 rates from day one. For properties in the Onion Creek corridor where sellers have held policies since before 2021, the gap between a seller’s grandfathered rate and what a new buyer will pay can be substantial. It’s a legitimate line item in any offer price negotiation.

The Flash Flood Reality Behind the Maps

Austin’s flood risk doesn’t look or behave like coastal flooding. No storm surge. No days of warning. No gradual water rise you can sandbag against. Austin’s floods are driven almost entirely by the Edwards Plateau—the shallow, thin-soiled limestone shelf to the west of the city that absorbs almost nothing when it rains hard. Water that falls on the Plateau moves fast into creek systems that can rise to dangerous flood stage with little warning.

Shoal Creek went from modest flow to eight feet of water in less than two hours during the 1981 flood. That’s the speed you’re dealing with.

The danger windows are spring and fall—roughly March through June and September through October. The 2013 Halloween flood that destroyed or severely damaged homes along Onion Creek followed a storm that delivered extreme rainfall in a matter of hours. The 2015 Memorial Day floods struck central Texas watersheds and caused widespread damage. These aren’t historical footnotes. They happened because of the specific hydrology of this landscape, and nothing about that hydrology has changed.

NOAA’s updated precipitation frequency data for Central Texas reflects increasing intensity of extreme rainfall events in the region. Local watershed engineers argue that current FIRM panels may already understate risk in some Austin corridors—that the maps are catching up to a reality moving faster than the modeling cycles. This matters particularly for buyers relocating from coastal metros who have developed intuitions about flood risk but not about flash flood behavior in a limestone watershed. The danger here isn’t the slow creep of water you can photograph from your porch. It’s a creek running eight feet deep with almost no warning.

Thousands of Austinites live safely near Onion Creek, Walnut Creek, and Shoal Creek. But buying near any of them without knowing your zone designation, your realistic insurance cost, and what sits upstream of your house is just not a good idea. The information is public and free. Use it.

Resources and Where to Get Help

FEMA Flood Map Service Center: msc.fema.gov — look up your FIRM panel number, zone designation, and any pending preliminary revisions

City of Austin FloodPro GIS Viewer: austintexas.gov/floodpro — the city’s Fully Developed Floodplain mapping for local permitting purposes

Austin Watershed Protection Department: 512-974-2550 — for questions about local panel status, pending LOMRs, and city floodplain standards

FEMA Community Numbers: City of Austin: 480624 / Travis County (unincorporated): 480625 — needed for NFIP applications and LOMA filings

Texas Department of Insurance: tdi.texas.gov — complaint filing, carrier licensing verification, and flood insurance guidance specific to Texas policyholders

Elevation Certificates and LOMA Support: Contact a licensed land surveyor and ask whether they have experience with flood zone work in the Austin-area corridors relevant to your property. Not all do.

Local Independent Agents: Ask any independent agent whether they write both NFIP policies and private market flood through carriers such as Neptune, Wright Flood, or Selective. Agents who place significant flood volume in Travis County will typically quote both and explain the trade-offs for your specific property.

If your property is in 78748, 78744, 78753, or 78754, start here: pull the current FIRM panel yourself at msc.fema.gov, open the same parcel in FloodPro, and ask a local independent agent for both an NFIP quote and a private market quote. If you’re in Zone AE, ask a surveyor what an Elevation Certificate would cost and whether your first-floor elevation makes a LOMA worth pursuing. The gap between what this costs and what it can save you is not close.