How to Read the FEMA Flood Map for Your Austin Property Before You Buy

FEMA's national map is the starting point. Austin's own floodplain viewer is where the real story lives. Most buyers never check it.

How to Read the FEMA Flood Map for Your Austin Property Before You Buy

FEMA’s national map is the starting point. Austin’s own floodplain viewer is where the real story lives. Most buyers never check it.

If you’re under contract on a house in Austin — or even just running searches on Zillow at midnight — the flood zone question deserves more than a glance at the disclosure form. Austin sits at the convergence of Gulf moisture, limestone terrain, and some of the fastest-rising urban creeks in the country. Its flood maps are more complicated than any single database captures. Here is exactly how to look up a property, what you’re looking at when you do, and what the numbers actually mean before you close.

Start Here: Run Both Lookups Before You Do Anything Else

Most buyers who think to check flood risk at all pull up FEMA’s national database and stop there. That’s a mistake in Austin. You need two URLs. Neither alone gives you the full picture.

austintexas.gov/floodpro is the City of Austin’s regulatory floodplain viewer, maintained by the Watershed Protection Department. It is the operative standard locally. When Austin’s map and FEMA’s map disagree about where a boundary falls — and they do, more often than you’d expect — Austin’s designation governs what you can build, where your finished floor must sit, and what the city will require of you.

msc.fema.gov is FEMA’s Flood Map Service Center, where you access the Flood Insurance Rate Maps (FIRMs) that determine federal insurance mandates and lender requirements. Your mortgage lender is looking here. Your NFIP insurer is pricing off this.

FEMA’s Special Flood Hazard Area designation triggers mandatory purchase requirements. Austin’s map goes further, including a 25-year floodplain designation that has no federal equivalent and is completely invisible on FEMA’s site. Run both. Screenshot both. Save them to the property folder you’re building.

Step-by-Step: How to Pull the Flood Designation for a Specific Address

Using Austin’s FloodPro Viewer

Go to austintexas.gov/floodpro. The interface is a GIS-based map with a search bar. Type the full street address. The map will center on the parcel.

On the left panel, toggle on all of the following layers:

- FEMA Effective Floodplain — The federally adopted 100-year (1% annual chance) flood boundary as FEMA has officially mapped it for Austin.

- Austin Regulatory Floodplain — The layer most buyers miss. The city’s own floodplain determination, which in many areas extends further than the FEMA boundary.

- Floodway — The high-velocity core of the floodplain, where development is most severely restricted.

- 25-Year Floodplain — A City of Austin designation covering the area with a 4% annual chance of flooding. FEMA does not map this. Austin does, and it carries its own development restrictions.

If the parcel sits within any shaded zone, note which layer triggered it. A property can fall outside FEMA’s 100-year line but inside Austin’s regulatory floodplain — which still subjects it to local permitting restrictions. Screenshot the result with all layers visible and the address confirmed in the search bar.

Using FEMA’s Flood Map Service Center

Go to msc.fema.gov. Under “Address Search,” enter the property address. FEMA will return the applicable FIRM panel. For Travis County — which covers most of Austin proper — the relevant FIRM panels fall in the 48453C series. Surrounding counties have their own prefixes; confirm you’re on the Travis County panel for city of Austin addresses. Note the effective map date and the panel number.

On the map panel itself, look for three things: the zone designation (AE, X, AE with floodway, etc.), the Base Flood Elevation (BFE) in feet above mean sea level if one has been calculated, and the FIRM panel number. The BFE matters most in Zone AE — it tells you the elevation at which the 100-year flood is modeled to reach. The panel number is what you’ll need if you ever pursue a Letter of Map Amendment or reference the map for an elevation certificate. Screenshot the panel map with the subject property highlighted, the zone designation visible, and the effective date in frame.

Before you finish, check msc.fema.gov for any pending map revisions affecting the panel. A “Preliminary” or “Pending” flag means the panel is under revision. A property showing Zone X today could be remapped into Zone AE at the next effective date — or vice versa. It happens.

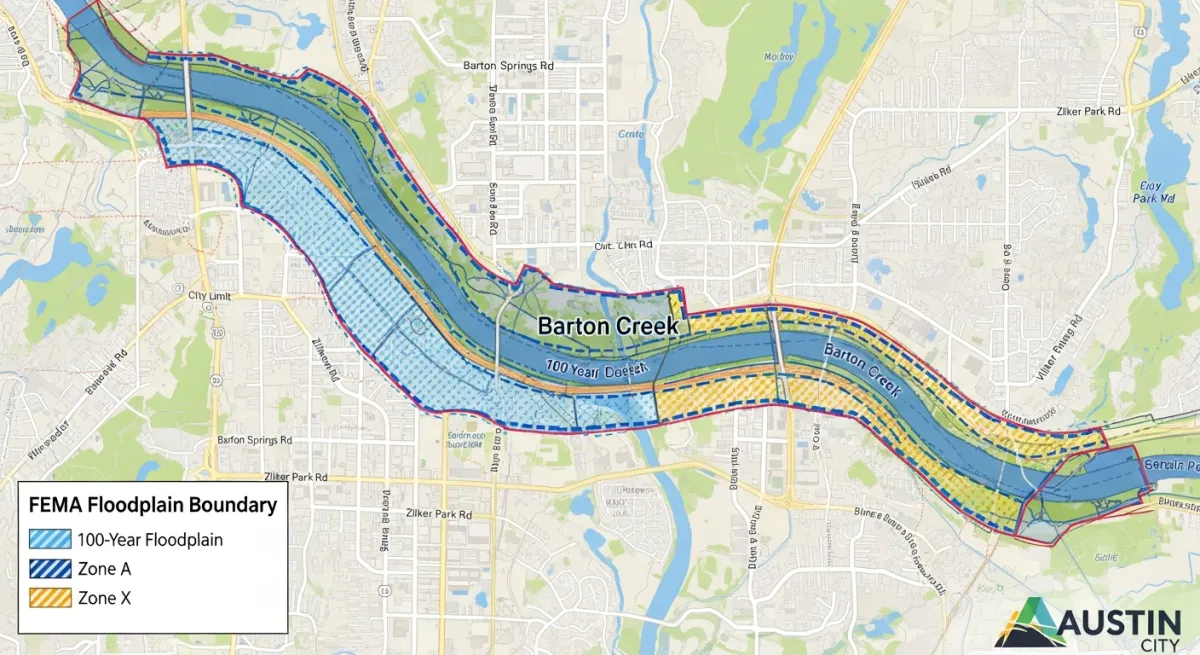

What You’re Actually Looking At: Zone AE, Zone X, Floodway, and the 25-Year Line

Zone AE

Zone AE is FEMA’s designation for areas within the 100-year floodplain where a Base Flood Elevation has been calculated. It’s the Special Flood Hazard Area designation that triggers mandatory flood insurance for federally backed mortgages.

In Austin, Zone AE runs along Shoal Creek through Hyde Park and Brentwood, along Barton Creek in Southwest Austin, and through significant stretches of Onion Creek in the southeast. If you’re looking at a property near the Shoal Creek corridor, or a home along Slaughter Lane near Onion Creek, Zone AE is what you’ll see on both maps. Mandatory flood insurance kicks in with a federally backed mortgage. Significant restrictions apply to what can be built or remodeled at or below the BFE. And Austin’s freeboard requirement — more on this below — means the city holds you to a higher finished floor standard than federal law requires.

Zone X (Unshaded and Shaded)

Zone X covers areas outside the mapped 100-year floodplain. Unshaded Zone X sits outside the 500-year floodplain entirely. Shaded Zone X — sometimes labeled Zone B on older maps — falls between the 100-year and 500-year boundaries.

No mandatory insurance. No federal development restrictions. But Zone X does not mean no flood risk. It means FEMA has modeled this location as having less than a 1% annual chance of flooding under current conditions. In Austin, that threshold has been exceeded — not hypothetically, but repeatedly and recently. The 2015 Memorial Day floods and the 2018 Halloween storm both put water into Zone X properties whose owners had no flood insurance and no warning in their disclosure paperwork.

Regulatory Floodway

The floodway is the inner channel of the 100-year floodplain — the area that must remain open to carry floodwaters without raising flood levels more than one foot. Development restrictions here are severe. You generally cannot fill, grade, or build structures that obstruct flow. Even a shed or retaining wall can require a floodway encroachment analysis. The Barton Creek corridor in Southwest Austin has some of the city’s most constrained floodway parcels. So does the lower reach of Shoal Creek through Pease Park. If FloodPro shows a floodway overlay on your parcel, treat that as a buildability constraint — not a footnote.

Austin’s 25-Year Floodplain

Most buyers have never heard of this designation. Most real estate agents haven’t either, frankly. Austin locally maps the area with a 4% annual chance of flooding — the 25-year storm event — and imposes its own development restrictions within it. FEMA doesn’t regulate this zone. It exists only in Austin’s local code and on the FloodPro viewer. A property that sits between Austin’s 25-year line and FEMA’s 100-year line may carry no federal insurance mandate and no FEMA restriction. The city can still limit what you build, require drainage studies, and apply setback rules. You will not find any of this on FEMA’s site.

The Part FEMA Doesn’t Cover: Austin’s Stricter Local Rules

Austin’s floodplain regulations exceed federal minimums in ways that matter concretely when you’re buying or building. As part of our home & property coverage, we’ve seen this trip up buyers at every price point — not because the rules are hidden, but because no one pointed them in the right direction.

The finished floor of a new structure in the 100-year floodplain must sit above the Base Flood Elevation by a locally required margin under Austin’s Land Development Code Chapter 25-7. FEMA’s minimum is zero — a structure with its floor exactly at BFE satisfies federal requirements. Austin requires more. That freeboard is both a safety buffer and a factor in insurance pricing: a structure elevated above BFE typically pays significantly lower premiums. If you’re buying an older home in a Zone AE area built before Austin adopted this standard, the lowest floor may sit at or near BFE. That’s a critical detail for your elevation certificate review. Confirm the current freeboard figure in LDC Chapter 25-7 or call the City of Austin Watershed Protection Department directly.

Austin also restricts development within the 25-year floodplain even though federal law is silent on it. This can affect additions, detached structures, impervious cover, and grading. A buyer planning to add a guest house or substantially expand a home in this zone needs to check with the Watershed Protection Department before assuming local permits will follow. Don’t find this out after you’ve closed.

The city also requires that development in or near the floodplain not displace floodwater onto neighboring properties. If you fill a low area or cut into a hillside, you must compensate with equivalent storage elsewhere on the site. This is stricter than federal rules and affects what is practical to build on sites with topographic complexity — which describes a lot of Austin.

For questions about what’s allowed on a specific parcel, pending map changes, or whether an existing structure complies: call the City of Austin Watershed Protection Department. Not FEMA. Not your lender’s flood desk.

”I’m Just Outside the 100-Year Line” — What Austin’s History Says About That

The reasoning is understandable. You ran the maps. The property is in Zone X. No mandatory insurance. Your lender isn’t requiring anything. Why spend the money?

Because in Austin, the 100-year flood line has been crossed by events that arrived fast and without apology.

The May 2015 Memorial Day floods hit parts of Central Texas within hours, overwhelming Onion Creek, the Blanco River, and several smaller Austin-area drainages. Properties mapped in Zone X went under. Some of those owners had no insurance. In October 2018, a Halloween weekend storm dropped 7 to 9 inches over Southeast Austin in a few hours. Onion Creek crested above its modeled 500-year level at some gauges. The 500-year floodplain — a boundary that by definition is supposed to flood once in five centuries under historical conditions — was not a meaningful protective designation that night. I don’t know how else to say that.

Austin’s geography explains why this keeps happening. The city sits at the edge of the Edwards Plateau, where limestone provides almost no natural infiltration. Rain that falls on the Hill Country hits impervious rock and funnels immediately into creeks — Barton, Shoal, Bull, Onion — that rise with extraordinary speed. Gulf moisture systems that stall over Central Texas produce rainfall totals that outpace what the models anticipated when those maps were drawn.

An NFIP preferred-risk policy on a Zone X property in Austin runs roughly $400 to $800 per year depending on structure and contents values. That is cheap coverage against an event Austin has demonstrated is not as rare as the map implies.

What Flood Insurance Will Actually Cost on an Austin Property

FEMA’s Risk Rating 2.0, which took effect in October 2021, replaced the old system that priced flood insurance primarily on zone designation and floor elevation relative to BFE. Under Risk Rating 2.0, NFIP pricing reflects the specific property’s flood frequency, flood depth, distance to water, and reconstruction cost. Two houses on the same Zone AE block can carry very different premiums. This surprises buyers who assumed they could ballpark the cost from a neighbor’s policy.

A Zone AE home in the Onion Creek corridor with the lowest floor at or below BFE can carry annual NFIP premiums anywhere from $2,000 to well above $4,000, depending on flood history and elevation. That figure drops substantially if the lowest floor meets Austin’s local freeboard standard — a property sitting above BFE might see rates closer to $800 to $1,500. The difference is real, and it’s one of the concrete financial arguments for Austin’s stricter local standard. Shaded Zone X properties with preferred-risk coverage have historically run $400 to $800 for building and contents, though Risk Rating 2.0 is pushing some of these higher for properties with elevated risk characteristics.

Before you finalize a purchase on any Zone AE property, get an elevation certificate. This is a surveyor-prepared document recording the lowest floor elevation, lowest adjacent grade, and other structural measurements relative to the BFE — the document your insurer uses to calculate your premium. A seller may have one on file; ask your agent to request it from the disclosure materials. If none exists, budget $300 to $600 for a licensed surveyor. This is money well spent. A property sitting above BFE without a certificate will be quoted worst-case rates until the certificate proves otherwise. Don’t let that happen at the eleventh hour.

The City of Austin participates in FEMA’s Community Rating System, which rewards communities that exceed minimum floodplain management standards. CRS participation generates a discount on NFIP premiums citywide. Confirm Austin’s current CRS class and the corresponding discount percentage with the Watershed Protection Department or the FEMA CRS database before closing.

On private flood insurance: several carriers are actively writing policies in Texas — Neptune, Palomar, and various surplus lines writers among them. On Zone X and some Zone AE properties they can price below NFIP, sometimes significantly, with faster claims handling and higher coverage limits. The tradeoff is that private policies lack the federal backstop guaranteeing NFIP’s claims payment. In a catastrophic regional flood — the kind that wipes out hundreds of properties at once and strains carrier capacity — that distinction matters. Get a private quote alongside your NFIP quote. Just don’t assume cheaper automatically means better here.

How Often Austin’s Flood Maps Change — and What That Means for What You Buy Today

FEMA’s Risk MAP program continuously updates Flood Insurance Rate Maps as watershed studies are completed, post-disaster analyses come in, and infrastructure projects alter drainage patterns. Travis County FIRM panels — the 48453C series — have been revised multiple times and will be revised again. Map changes run both directions. A Zone AE property can shift to Zone X if a flood control project reduces risk. A Zone X property can be remapped into Zone AE if a revised study shows higher risk than previously modeled.

The Waller Creek Tunnel is the clearest recent example. The tunnel diverts Waller Creek floodwaters, reducing flood risk along the corridor through East Austin and the UT area. FEMA subsequently issued a Letter of Map Revision that changed designations along parts of the corridor — some properties that had carried mandatory flood insurance for years ended up in Zone X. But the process was slow. There were years between tunnel completion and the final effective map revision, and the uncertainty during that window was real and financially meaningful for owners trying to sell.

The Onion Creek buyout program cuts the other way. After the 2013 floods inundated the Onion Creek subdivision in Southeast Austin, the city and FEMA funded a buyout that eventually purchased and demolished several hundred homes in the highest-risk areas. Those lots are now green space. That buyout was an acknowledgment that the maps, for years, had understated the risk while families were living there. Worth sitting with.

To check for pending revisions on a specific FIRM panel: go to msc.fema.gov, search by panel number, and look for “Preliminary” or “Pending” status. The Watershed Protection Department also tracks pending changes and can confirm whether a revision affecting a specific parcel is in progress.

If You Think the Map Is Wrong: LOMAs and Their Limits

A Letter of Map Amendment is a formal determination from FEMA that a specific structure or parcel has been incorrectly included in a Special Flood Hazard Area — typically because the land actually sits above the Base Flood Elevation. Property owners and their surveyors can apply using elevation certificate data. FEMA approval lifts the mandatory flood insurance requirement for federally backed mortgages.

If you’re buying a Zone AE property and the elevation certificate shows the lowest floor well above BFE, a LOMA may be worth pursuing. Call the City of Austin Watershed Protection Department before filing anything with FEMA. They can tell you whether the city’s own regulatory determination would affect the analysis and whether any drainage conditions near the property complicate things.

One critical caveat, and I want to be direct: a LOMA removes the federal insurance mandate. It does not mean the property won’t flood. The 2015 and 2018 storms put water into properties that had LOMAs on file — properties FEMA had formally determined sat above the 100-year flood level. Those determinations were correct under the modeled scenarios. The storms simply exceeded the model. Buyers who obtain a LOMA and then drop their flood coverage because the mandate is gone are taking a risk that Austin’s recent history has made very concrete.

Austin’s Most Flood-Prone Corridors

Onion Creek, Southeast Austin. Some of the highest NFIP premiums in the city. The 2013 buyout program removed several hundred homes from the highest-risk blocks. Active development still exists in adjacent areas — treat any address within a mile of this creek as requiring both map checks, no exceptions.

Shoal Creek, Hyde Park to downtown. Zone AE runs the length of it. A 1981 flood killed 13 people along this corridor and remains the benchmark event for Central Austin flooding. Properties on or near Shoal Creek warrant particular scrutiny regardless of what the current map shows.

Barton Creek, Southwest Austin. Zone AE along the creek, plus the Barton Springs Contributing Zone adds a second layer of environmental and development restrictions on top of flood regulations. The combination can significantly limit what is buildable on affected parcels — buyers planning additions often discover this later than they should. Understanding what home improvements actually add resale value in Central Texas is especially relevant here, where flood and environmental rules can make planned projects unbuildable after closing.

Waller Creek, East Austin and UT corridor. Post-tunnel map revisions changed some designations, but the remapping process has been gradual. Some sections remain in active revision. Confirm the current effective designation and check for pending changes specifically for this corridor.

Bull Creek, Northwest Austin. AE designation at the lower reaches near the Lake Austin confluence. Properties in adjacent neighborhoods sit near sensitive terrain.

Tributaries feeding Williamson Creek and the East Riverside corridor. Less prominent on the flood risk radar, but responsible for significant localized flooding during intense events. The 2018 Halloween storm hit this part of Southeast Austin hard and caught a lot of Zone X owners off guard.

Your Pre-Closing Flood Checklist

Pull this out when you have a property address and a contract in hand.

-

Run both maps and save the results. FloodPro with all relevant layers on; FEMA’s MSC with panel number and zone designation visible. Screenshot both with the address confirmed in frame. Note any discrepancy between what the two maps show.

-

Request an existing elevation certificate from the seller. If none exists on a Zone AE property, budget $300 to $600 for a licensed surveyor before you waive the option period. The certificate confirms the lowest floor elevation relative to BFE and directly affects insurance pricing.

-

Get insurance quotes before you commit. Contact an independent agent who writes both NFIP and private flood. Get at least one of each. On Zone AE properties this number can affect whether the purchase pencils.

-

Ask your title company whether any LOMAs or LOMRs are on file for the property. These affect the legal flood zone status and the seller’s insurance history. A previous LOMR that mapped the property out of AE may be pending revision back in.

-

Call the City of Austin Watershed Protection Department. Ask about pending map revisions affecting the parcel, and confirm what Austin’s local rules — not just FEMA’s — permit you to build or modify on the site. Do this especially if you have renovation plans.

-

If you’re in Zone X, get a preferred-risk quote anyway. The premium is low. Austin’s flood history is not reassuring on this point.

-

Buy flood insurance early. You don’t have to wait for closing. A policy purchased in the first week of escrow means you’re not scrambling in closing week with a coverage gap before the effective date.

The flood maps are not a guarantee. They’re a snapshot of modeled risk based on data that Austin’s weather has outpaced more than once in the past decade. Running both lookups — FloodPro and FEMA’s MSC — gives you the most complete regulatory picture available before you commit. What you do with that picture is your call. But you should at least be making it with the right information in front of you.

Questions about a specific parcel’s flood designation can be directed to the City of Austin Watershed Protection Department. Insurance premium figures cited here are illustrative; verify with a licensed independent insurance agent familiar with the Austin market.